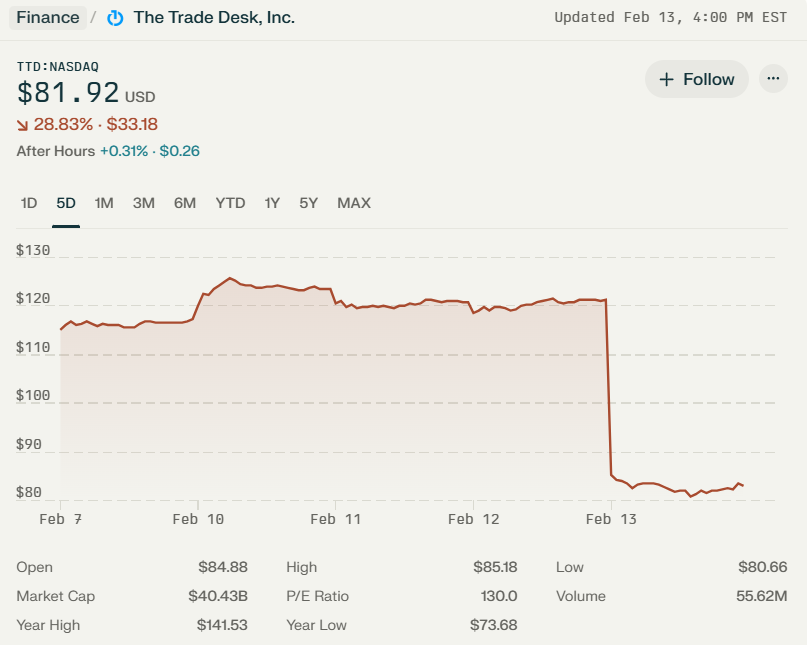

This is not a good chart:

The Trade Desk’s share price has plunged by about one-third (!) since yesterday’s disastrous Q4 earnings call. The company reported $741 million for the quarter—well below the expected $756 million—marking its first earnings miss in 33 quarters.

When explaining the shortfall, CEO Jeff Green attributed it to “small execution missteps,” while repeatedly emphasizing that the company has “a championship-caliber team” that just fumbled the ball a few times.

To Green’s credit—or detriment—he then outlined a 15-point plan to recover, which some have criticized as throwing “spaghetti at the wall.”

Why This Matters:

The Trade Desk has long been the adtech market’s public darling. But a miss and a drop of this magnitude shakes confidence—not just in the company, but in the broader adtech market, which had been riding fairly high until now. The first question is: What happened to The Trade Desk? The second: Is this a sign of a larger market trend?

Weirdly, though, this seems fairly isolated to The Trade Desk. While TTD’s stock was dropping 30% after a rough earnings call, AppLovin—on the performance side of the industry—saw its stock surge 30% after a standout report. The contrast hasn’t been lost on the industry, with some seeing it as proof that The Trade Desk’s “premium internet” pitch isn’t as compelling as the “performance internet” that AppLovin is focused on.

Meanwhile, on the CTV side, Roku just reported stellar earnings, reinforcing the strength of a market The Trade Desk has long benefited from. (Roku claps back, I guess.)

You also have to imagine that other DSPs—Yahoo, Basis, Viant—are licking their lips a little (maybe even the bigger guys like Amazon), realizing that The Trade Desk “is human” and, at least in theory, can be taken down.

Experts React:

Here are some of the most interesting tweets about the Q4 numbers:

Our Take:

We tweeted about this last night:

One of the most interesting takeaways from The Trade Desk’s prepared remarks was its heavy focus on “supply chain” optimization—highlighting its work with newly acquired Sincera and OpenPath. But this feels like nibbling around the edges rather than a compelling narrative like “we’re dominating CTV” or “we’re leading the retail media boom.” Do investors care about a clean supply chain? Do they understand the value? Probably not.

A big part of The Trade Desk’s success with investors, shareholders, and prospective investors has been its ability to tell a clear, easy-to-understand story: These two high-growth opportunities are taking off, and we’re at the center of it. Grow with us. But with increasing competition and market clutter, that story is becoming harder to own.

Shifting the pitch to “auction mechanics” and supply path optimization (SPO) feels like The Trade Desk is positioning itself as just another adtech company, not a category-definer. Though, to be fair, this could be where Ventura comes into play as it’s a big bet.